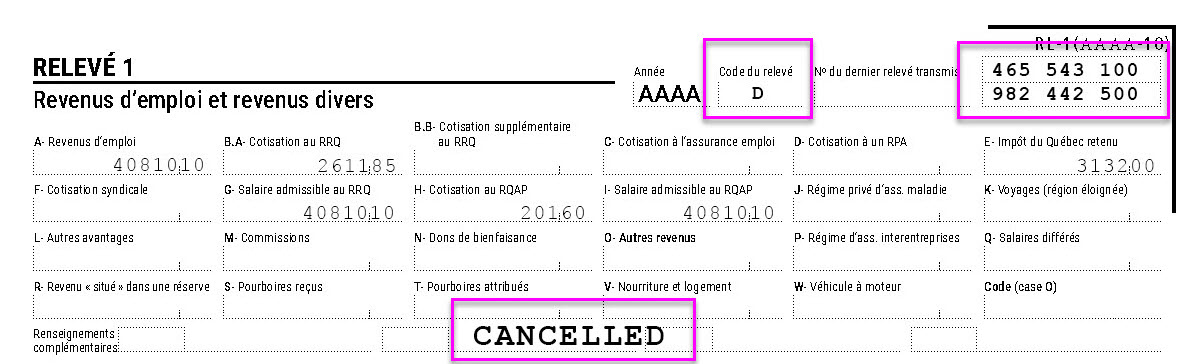

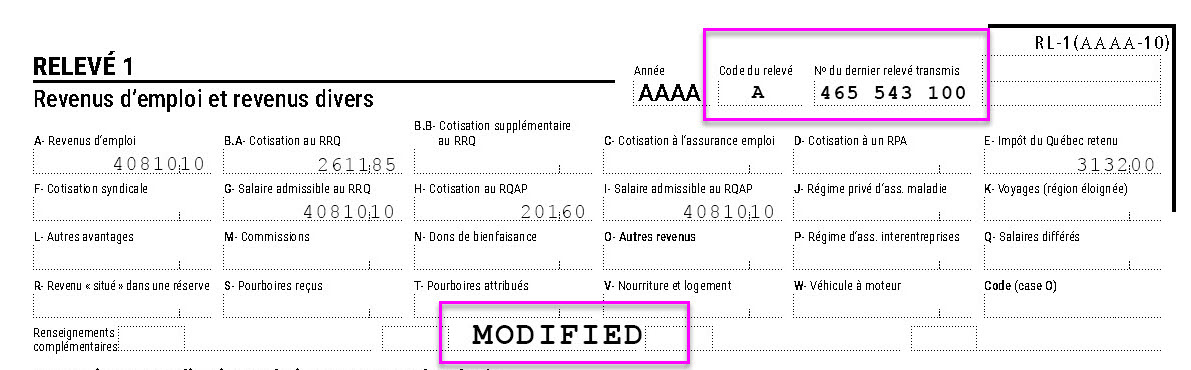

✓What is it?

⇨The enhancement first came into effect in 2019, to provide future retirees with a higher retirement income.

⇨Between 2019 and 2023, in addition to base contributions under the QPP and CPP, employers were required to deduct a first additional contribution on the portion of earnings eligible for the QPP/CPP for the year.

⇨Since January 2024, in addition to the base contributions and the first additional contribution deducted up to annual maximum eligible earnings of first ceiling, a second additional contribution is deducted up to maximum eligible earnings of second ceiling.

Please refer to the table below for 2025 rates and maximums.

2025 QPP/CPP rates and maximums

|

Deductions

|

Rate

|

Maximum

eligible earnings

(first ceiling)

|

Maximum

eligible earnings

(second ceiling)

|

Basic exemption

|

Maximum

contributory earnings

|

Maximum contribution

|

QQP - Base and first additional

contribution

|

6.40%

|

$71,300

|

|

$3,500

|

$67,800

|

$4,339.20

|

QQP - Second additional

contribution

|

4.00%

|

|

$81,200

|

|

$9,900

|

$396.00

|

Total:

|

|

|

|

|

|

$4,735.20

|

|

|

|

|

|

|

|

CPP - Base and first additional

contribution

|

5.95%

|

$71,300

|

|

$3,500

|

$67,800

|

$4,034.10

|

CPP - Second additional

contribution

|

4.00%

|

|

$81,200

|

|

$9,900

|

$396.00

|

Total:

|

|

|

|

|

|

$4,430.10

|

✓Which employees contribute to the additional CPP/QPP plan?

Employees with income that exceeds the maximum eligible earnings for 2025 ($71,300). This second additional contribution is calculated on earnings between the first and second earnings ceiling eligible for CPP/QPP calculations and must not exceed $396.00 ($81,200 - $71,300 x 4.00%).

✓Where can you find this information?

o In your reports:

Contributions to supplementary CPP and QPP plans are included in basic CPP (D10) or QPP (D1) deductions. These can be viewed in the Payroll record - SPD603 and Agencies remittances - SPD615 report.

o In the web payroll application:

Contributions to supplementary CPP and QPP plans are displayed in the Quantity column of the employee’s year-to-date total (Employee file > Employee >History > Year-to-dates).

–The amount shown in the Quantity column appears when the first QPP contribution limit is reached. It represents a second contribution ceiling for the organization.

–If the maximum has not been reached, the number in the Quantity column is 0.

For more information, please visit the Canada Revenue Agency or the Retraite Québec websites. For more information, please visit the Canada Revenue Agency or the Retraite Québec websites.

|